Minimum Alternate Tax Mat Pdf

Minimum Alternate Tax

Minimum Alternate Tax Tax Credit Tax Deduction

Mat Vs Amt Minimum Alternate Tax And Alternative Minimum Tax Vakilsearch

Title Minimum Alternate Tax Mat Author Ca Kamal Garg Publisher Bharat Law House 6th Edition 2017 Type Paperback Vorabookh Vora Books Bookstore

Minimum Alternate Tax In India A Comparative Analysis Of Provisions Under Income Tax Act And Direct Tax Code

Guide To Minimum Alternate Tax For Ind As Compliant Companies

Introduction as the book profit based on ind as compliant financial statement is likely to be different from the book profit based on existing indian gaap the cbdt constituted a committee in june 2015 for suggesting.

Minimum alternate tax mat pdf.

All About Alternate Minimum Tax Amt Section 115jc

Https Www2 Deloitte Com Content Dam Deloitte In Documents Tax In Tax Minimum Alternate Companies Noexp Pdf

Https Papers Ssrn Com Sol3 Delivery Cfm Ssrn Id1759907 Code1612178 Pdf Abstractid 1759907 Mirid 1

Ca Final Question Bank Dt Minimum Alternate Tax Mat

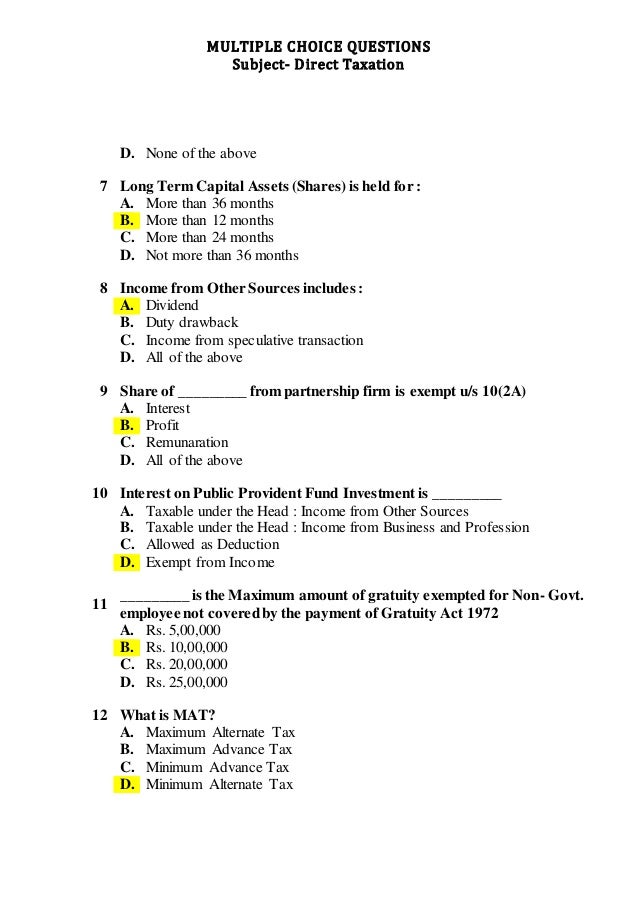

Multiple Choice Questions On Direct Taxation

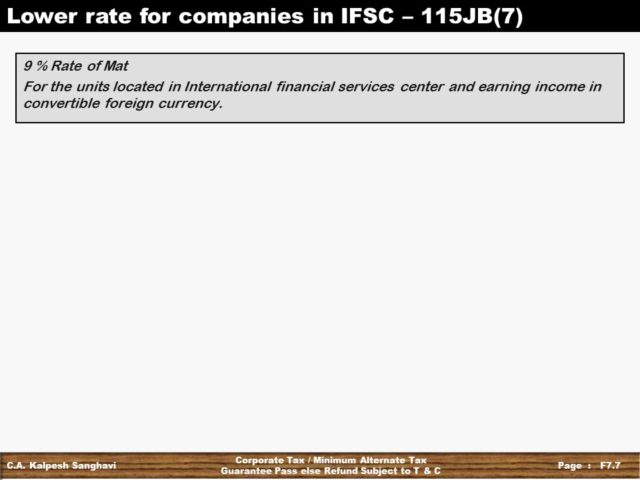

Minimum Alternate Tax Mat Section 115jb

Explained What Is Minimum Alternate Tax Or Mat

Memory Technique Minimum Alternate Tax Section 115jb May Nov 2019 Attempt Youtube

Mat Vs Amt Minimum Alternate Tax Alternate Minimum Tax Indiafilings

Incometaxindiaefiling Gov In Efiling Portal Staticpdf Response Defective Return Pdf Income Tax Math Portal

What Is Minimum Alternate Tax Mat News Budget 2020 News Mat Calculation

What Are The Recommendations For Union Budget 2019 Suggested By Aiftp

Pdf Goods And Service Tax A Detailed Explanation With Examples Taxguru In Goods And Service Tax Goods Service Tax Detailed Explanation Examples Html Thirupal Gandhudi Academia Edu

Difference Between Mb Ib Investment Banking Banks

Calculation Of Mat Credit Applicability Of Minimum Alternate Tax

Pdf Algorithm For Calculating Corporate Marginal Tax Rate Using Monte Carlo Simulation

Minimum Alternate Tax For Companies Indiafilings

Pdf Budget Terminology Rose M Academia Edu

Government Notifies The Direct Tax Vivad Se Vishwas Rules 2020 And Corresponding Form

Https Www Singtel Com Content Dam Singtel Investorrelations Stockexchange 2020 Balrelease 20200730 Pdf

Download Pdf Ca Final Direct Tax Important Questions Nov 2019 Income Tax

Current Income Tax Rates For Fy 2019 20 Ay 2020 21 Sag Infotech

Corporate Tax In India Overview Rates Tax Liability

Pdf Emerging Trend In Indian Direct Taxation An Analysis Of Income Computation And Disclosure Standards

Source : pinterest.com